Data stewardship and minimum data standards in reinsurance

While we possess more computational power and analytical sophistication than at any point in reinsurance history, the key challenge of the industry as it stands remains the reliability of risk information. Indeed, we are at a point where human expertise is not being replaced by technology, but rather seamlessly integrated with agentic systems. We're dealing with autonomous AI entities that are capable of working with and making complex risk infrastructures, workflows, and micro-decisions without constant intervention.

And so we have another very important thing to think about here, because the efficacy of these agentic systems is entirely dependent on the quality of their fuel, AKA, data.

Data in reinsurance

As noted, there is a transition happening, taking reinsurers from prediction-led models to resilience-informed risk management. With this in mind, it seems silly to suppose we can simply attempt to forecast the ‘unforecastable.’ Instead, reinsurance leaders need to think more along the lines of building systems that are inherently resilient, adapting to shifting data environments in real-time.

And so, when it comes to data, we're talking about reframing the concept of ‘digitisation’ from something of a solely technological matter to something which requires really quite a lot of stewardship. Stewardship? What's that got to do with us?? Well, indeed, if you look at how things have been done historically, but as everyone is saying, and I'm afraid it is the truth, things are changing.

In 2026, data governance must be treated as a product and a vital operating constraint. It is the framework that ensures an organisation's digital nervous system can communicate effectively with cedants, retrocessionaires, and automated markets. Without that commitment to minimum data standards (MDS) and active stewardship, AI-driven efficiency simply will not be.

Let's start with minimum data standards

For over a decade, the benchmark for data quality in the European and UK markets was dictated by Solvency II technical provisions, which mandated that data must be "appropriate, complete, and accurate”. While this triad remains foundational, it represents a retrospective, static view of risk. That is, ensuring the data is clean enough for legal reporting, but not necessarily agile enough for modern operational environments.

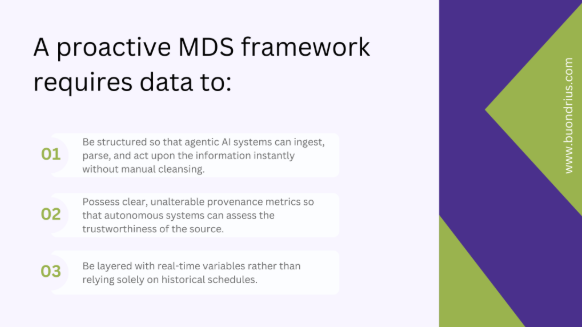

What ought to happen next in reinsurance is that leaders should take steps towards a proactive MDS framework which goes beyond mere regulatory correctness.

One of the greatest operational friction points I've seen is the sheer volume of fragmented disclosure requirements. Reinsurance carriers seem to be caught in a crossfire of overlapping sustainability and financial regulations across the EU, the UK, and Switzerland, which has triggered severe corporate reporting fatigue.

The root cause of this fatigue is granularity. Particularly regarding Scope 3 emissions data. As the University of St.Gallen’s report highlights, and as I've generally spoken about quite a bit in my bordereaux report, much of the corporate sustainability data provided by cedants remains highly unreliable and poorly standardised.

The solution

Well, it's surely clear that reinsurance leaders cannot solve reporting fatigue by asking for less data! No, they must solve it by demanding better structured data at the point of inception.

Thus, digitisation strategies should enforce an MDS that captures data at the highest possible level of granularity right at the underwriting submission stage. By capturing raw, highly granular risk characteristics rather than aggregated summaries, automated data pipelines can be used to map a single data set to multiple regulatory outputs. This protects cedants from repetitive data requests while providing underwriting agents with the high-fidelity information they need to price complex risks accurately.

Data stewardship and agentic AI

For reinsurance leaders looking to capitalise on these autonomous technologies while mitigating systemic risk, three immediate, actionable mandates should be prioritised.

Mandate interpretability metadata within your minimum data standards (MDS). Every data pipeline feeding an underwriting agent must include verifiable tracking that allows human underwriters to audit why an agent reached a specific pricing decision or risk aggregation threshold.

Move away from proprietary, siloed data frameworks. Use your position to establish market-wide coalitions that standardise risk reporting formats.

Appoint dedicated data product owners within underwriting units. These individuals are responsible for the quality of specific risk data assets. They must ensure it meets both internal machine-learning requirements and external regulatory standards.

At the end of the day, it's been said before, and I'm sure it'll be said many more times to come, given the way things are going with AI and technology: data integrity is foundational to any form of commercial resilience. And how do we achieve data integrity? Through active data stewardship and enforcing rigorous minimum data standards.

I’ve been supporting companies with their digital challenges for over 27 years now. If you’d like to know more about data and what standardisation could look like in your business, do get in touch and let’s have a chat.

Sources: